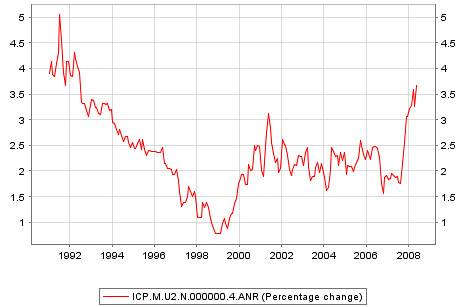

Inflation is here to stay

Written by A Forex View From Afar on Monday, June 30, 2008Back to www.thelfb-forex.com

The Bank for International Settlements – the central bank of central banks – has released the annual report regarding their global economic outlook.

The BIS reconfirmed what the market already knew, that central banks have to choose between inflation fighting and assuring growth, and they also they pointed out some of the causes that led to the excessive credit build up.

Perhaps the principal conclusion to be drawn from today’s policy challenges is that it

would have been better to avoid the build-up of credit excesses in the first place. […]Recognising that cycles can be attenuated but not eliminated, a number of preparatory steps are also suggested that would allow periods of financial turmoil or crisis to be more effectively managed.

Remember the 1% rate on Fed Funds for over 1 year? Does that spark a thought of where we are right now? It was only 6 years ago. This is why expectations play a very important role in macroeconomics. It takes a lot of time to steer the economy through a central bank’s leverages, and they are: the interest rate, their reserve requirements, and the discount window that they service with cheap loans. The median times can be anywhere from 6 months to 18 months to get an economy back on course.

The slow response of the economy means that a central bank must act in a proactive fashion, something that central banks were not able to do recently, due to the tight credit conditions (= credit crises). Hesitation will now play its role in the coming months in the form of inflation.

I won’t accuse anybody here, since monetary authorities had a good reason to keep rates on hold or even cut, but when we have a central bank that cuts for the market’s sake, this means that problems are lying ahead, we now have the pay-back from emergency rate cuts, and that is in the form of inflation and soring commodity inflation because of a low U.S. $

Well, the BIS somehow supports my view by saying:

In the aftermath of a long credit-driven boom, it would not be surprising to see turmoil in financial markets, slowing real growth and temporarily rising inflation.[…] At the same time, inflationary forces, particularly in emerging market economies, could also prove unexpectedly strong and persistent. A major factor in inflation prospects everywhere is likely to be the behaviour of wages, but in some countries the effect of a depreciating exchange rate on domestic prices could also play an unwelcome role.

Hmm, depreciating exchange rate? Is the Fed or the Treasury hearing this???

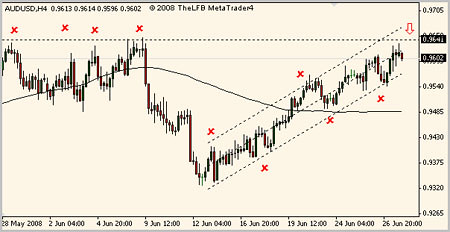

My personal conclusion is that inflation is here to stay and is definitely more then a bump in the CPI charts, and at the same time global growth is very likely to slowdown. If the dollar is set to fall it means that the oil is set to rise, global growth slow-downs are not going to impact the oil demand it seems, not all of the time that China and India are stock-piling, and definitely not when Iran is at the center of a political storm. There is no easy answer, except maybe that the 4 hour chart channels may be are new best friend over the summer, the alerts posted on TheLFB cover what to look for. Ready? Up, down, up, down, up, down.......

| Posted in »

| Posted in »