Written by A Forex View From Afar on Saturday, May 17, 2008

Back to www.thelfb.com

2 bubbles have burst in less than a decade- the 2000 Tech Bubble and 2007 Housing Bubble, now the 3rd one is forming: the commodity bubble

Since September 2007 global Commodities Indexes have gained between 40% and 70%, putting additional pressure on consumers who are suffering higher prices. Some will argue the supply/demand relationship triggered this rise, saying there is no bubble because inventories have not increased- pure supply and demand drivers. While others will argue that commodity price gains are a consequence of the loose monetary policy of the previous year. The Indian and Chinese stockpiling of energy is something to bear in mind, because the average price that they will have on a barrel of Oil may seem very expensive if we see a pull-back. That could add to the reversal momentum when it does come.

The important part is that Oil prices are affecting our limited consumer pockets, and something may have to be changed in Fed’s mentality of ignoring inflation and concentrating on growth. A low value Dollar may be what is required to create a Jump-Start, but by doing so it is allowing a Bull run in Oil to turn into a stampede. By every possible standard, two bubbles and 8 years is huge, not to speak about the newly forming one- Commodities.

Last week gave the perfect opportunity for Fed official to make a public move that could have helped the consumer, and their battle with Gas and energy prices. First, as some part of the media covered, was the change of attitude over Bubbles.

The Fed’s view was that they can’t stop bubbles from forming because they are too hard to be spotted in real-time, and even if they are spotted, by every means it should avoid monetary policy to stop them.

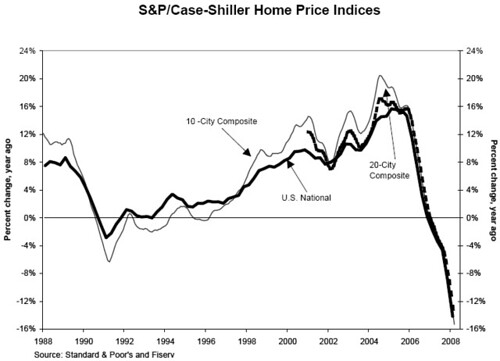

WSJ journal provides a chart of the recent bubbles. A 5th grader could see something wrong in those chars, especially in the Las Vegas prices, were prices increased exponentially, forming an almost vertical line.

Going further with the Fed’s view- monetary policy shouldn’t be used to stop the bubble, but it should be use to heal the economy once the bubble burst. Unfortunately, until now, they have only managed to create another bubble.

Usually, bubbles are created by inaccurate monetary and fiscal policies. To correct a fiscal policy is an almost impossible job, it takes months (if not years) for a law to be passed and a lot of time until is implemented. A monetary policy however needs no more than a few hours to impact, the market effect is almost instantaneous.

Higher interest rates, to stop a forming bubble, will mean the economy will slow, maybe the unemployment number will rise too, which is against Fed’s policy, so intervening while a bubble is forming seems very unlikely. This is why virtually all major Central Banks have one role: fight inflation. That is except the Fed.

In last week’s Fed Speeches some members started to discuss their rethinking on this policy, non-intervention while Bubbles are forming. It is a welcome step forward for the Fed, which we should be pretty proud off. You know, you first have to admit to have a problem, in order to solve it

"Hello everybody. My name is Fed, and I'm a bubble-holic".

The other big shift in policy that was seen last week in the Fed’s speeches was Mr. Bernanke trying to urge Congress to pay Interest on reserves sooner than 2011, when the Fed would normally start too. Always bear in mind that the Fed is not a Central bank, it is a private company that holds the Government check book, and therefore holds the taxpayers money, (for safe keeping of course). But unlike any other major region, the Federal Reserve is a private business that charges the Government for the task of holding, printing and counting (oh no, forget counting, the Fed scrapped Money supply numbers- "too costly to produce". Obviously cut into the private business profit line) the taxpayer's money.

Banks are required to keep a percent of their deposits in the Fed safe-fault, on which the Fed does not pay Interest, although other Central Banks do. Over time, paying Interest was proven to be very effective. Some academic papers suggested that the big difference on how the Fed and ECB handled the sub-prime lay in other bank’s reserves at their Central Banks. At the time when the Sub-Prime crisis began European Banks had 10 times more reserves at the ECB then US Banks at the Fed, and only because the ECB pays interest on those deposits, and encourages banks to save.

Sound familiar? The US income to expenditure rate is negative, the US, and the Fed, does not encourage saving- who needs it when a line of credit is always available? Or not, maybe. Lesson learned, rainy day savings are not just 401k's and Roth IRA's, the Stock market is for investment and asset appreciation over time, savings accounts and low credit card bills are what the Fed could teach by paying interest and setting rates that will tackle the overdrawn Government checking account. Lead by example maybe, rather than leading by looking for profit first. But as a private business the profit line maybe comes before the winning line, who knows? back to the point at hand..

Paying no interest, as is the Fed policy, makes banks hold no more than are legally required, with any and all cash surplus then lent to other banks, usually underneath the Fed Funds rate (Discount Window), which puts additional and unwanted pressure on the system. This pressure can be very bad, especially when the Central Bank, in our case the Fed, is in rate hike cycle. Banks borrowing under the Fed Funds sends rate down, while the Fed needs them up to be able to fight inflation.

Roll on paying Fed Interest, it may lead to a system in place and a thought process that comes from it to know that we need a savings umbrella to weather the stormy times. We can all learn from the Fed's lesson, and hopefully sooner rather than later.

Source:

WSJ: Fed and Bubbles: First, Heal Thyself?

| Posted in »

| Posted in »